By James Schulze

This article discusses some of the trends that support a positive outlook for the mortgage industry in 2026. It also discusses how lenders and brokers can best focus their lead generation resources to capture this opportunity.

After a tough stretch, the mortgage industry is showing some positive signs of life headed into 2026. Economic indicators are encouraging, creating greater stability. The housing supply is growing. And new regulations may boost long-term supply and affordability. All of these and more hint that 2026 could be a strong year for lenders and brokers.

Factors creating a more optimistic outlook for the mortgage industry

Some of the most important trends that are driving optimism in the mortgage market include:

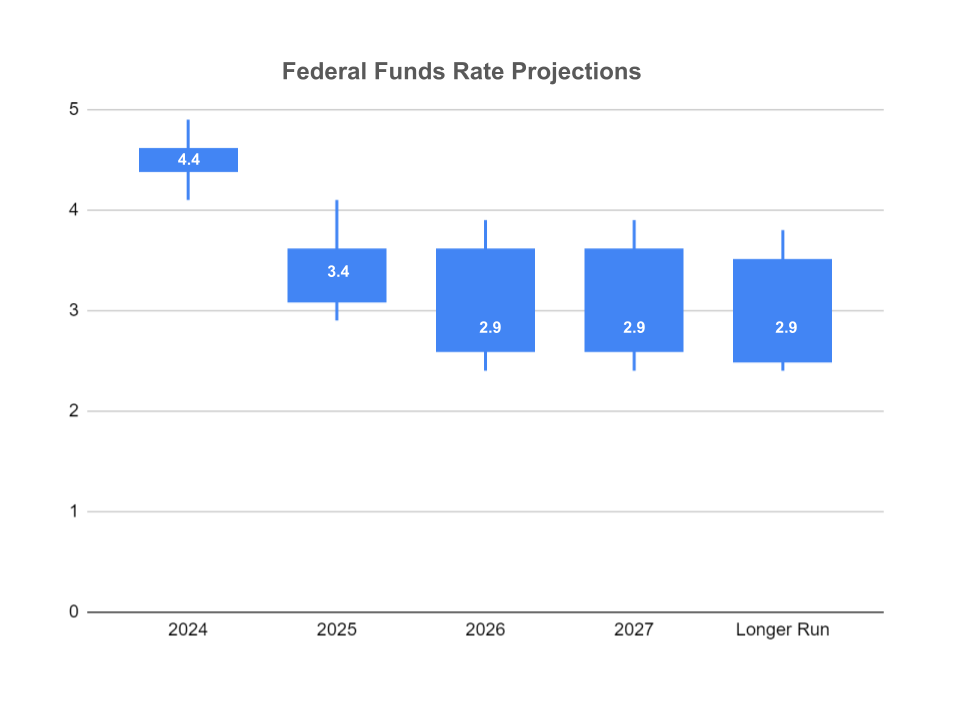

- Reduced inflation and lower interest rates – In February, the U.S. Bureau of Labor Statistics reported that the Consumer Price Index increased 2.4% over the 12-month time period ending in January 2026. It was 2.7% just one month earlier. Inflation figures are finally approaching low levels we haven’t seen for five years, before inflation ultimately spiked to 9.1% in June 2022. This is great news for American consumers, but also for mortgage lenders and brokers. When inflation cools, the Federal Reserve has less of a reason to keep the Federal Funds Rate high. It has reduced its rate three times over the last six months, settling in at a target rate of 3.50% to 3.75%. Many analysts expect this rate to be gradually reduced by at least another 25 basis points by mid-2026. When the Federal Funds Rate is lowered and treasury yields fall, mortgage rates also typically decline. A 0.75% to 1.00% drop in mortgage rates can significantly change borrower mentality, spurring both refinancing and purchase originations.

- More housing inventory – The number of home listings has increased 3.2% over last year. More sellers are putting their homes up for sale, shifting more power to buyers as they evaluate several options in the marketplace. Although homes are sitting on the market a bit longer, more inventory usually leads to more mortgage activity.

- Declining list prices – A Realtor.com study reported that the median list price of homes has decreased 2% year over year. In the fourth quarter of 2025, nearly 1 in 5 new homes (19.3%) were offered at a price reduction. Lower home prices might be just the incentive buyers need to move forward in purchasing a home and taking on a mortgage.

- Re-emergence of refinancing – Refinancing took a back seat while mortgage rates were high. Many homeowners chose to use home equity lines of credit (HELOCs) instead of refinancing. Compounding the problem, more and more homeowners are facing financial stress. Mortgage delinquencies rose 18.6% over the last year. With inflation now stabilizing, borrowers who are highly sensitive to monthly payments will likely be revisiting their options.

- Housing for the 21st Century Act– The mortgage industry may get a boost from recently developed legislation. In February, the House nearly unanimously passed the Housing for the 21st Century Act. It seeks to better align federal housing policy with the current economic conditions in the U.S. It aims to increase housing supply, stabilize communities, and make housing more affordable to Americans in both urban and rural markets. It should reduce regulation, speed up approvals, and expand access to financing. And while it won’t necessarily change the market overnight, it does indicate a long-term confidence in the housing market. All good for the mortgage industry.

Some regions offer even greater opportunities

While the mortgage industry seems poised to grow throughout the U.S., there are some areas that present very strong opportunities:

- Southeast– In cities such as Miami and Orlando, housing supply is particularly strong, as is buyer leverage. More listings means more opportunities to sell mortgages.

- Midwest– Housing in cities such as Kansas City and Indianapolis remains affordable. Value markets like these can offer steady loan volume.

- Texas– Housing inventory is expanding in Houston and Austin.

- California– California is one of the least affordable housing markets in the U.S. One estimate states that buyers need nearly half their income to afford even a median-priced home. This creates significant financial pressure, but for lenders and brokers, it also creates substantial demand for refinancing and HELOCs.

How mortgage lenders and brokers can pursue this opportunity

With such strong opportunities emerging, strategic-minded lenders and brokers will begin preparing for growth. And it all starts with identifying, targeting, and connecting with interested consumers. For many lenders and brokers, the most viable option for lead generation is purchasing aged mortgage leads. Aged leads are:

- High intent– Many consumers paused their home ownership aspirations in the last few years due to high mortgage rates. Several existing homeowners have been delinquent in making their mortgage payments but felt refinancing was not an option with high rates. Aged leads represent consumers who have already expressed interest in a mortgage or refinancing in the past year or so, but may not have taken action. They may now be ready to have a conversation about a mortgage or refinancing.

- High volume– Aged leads have the highest lead volume of any other type of opt-in lead. With more housing listings, there will be even more buyers who are looking for mortgages. Aged leads are perfect for call center operations and scaling your business.

- Cost effective– Aged leads are priced lower than any other type of lead, but they are still highly effective. Many lenders and brokers using aged leads realize higher margins and improved ROIs.

- Perfect in a cautious buyer environment– Buyers will likely continue to be cautious, not understanding exactly where the housing market is going. But they are not walking away, as evidenced in recent reporting. They will remain sensitive to housing prices, mortgage payments and rates. High pressure sales approaches do not always work well in a cautious market. Aged leads can be used very effectively with an educational sales approach. Well-timed, follow-up conversations are often more successful than a new-inquiry conversation in this environment.

As the market conditions and pending legislation takes hold, more homes will be on the market and more American consumers will be looking to buy homes or refinance their current home. Forward-thinking lenders and brokers will begin to prepare now and buy aged leads while the competition is lighter. Are you ready to get started strengthening your 2026 sales pipeline?

If you would like more information on how you can grow your mortgage sales, give The Leads Warehouse a call at 1-800-884-8371 or visit our website at http://theleadswarehouse.com

Related Post

Why Is It So Hard To Connect With Prospects Today?

By James Schulze This article discusses the different rules...

Federal Funds Rate Projections Are Good News For The Mortgage Industry

By James Schulze This article discusses the Federal Reserve’s federal...

Aged Mortgage Leads – Suggested Scripting #2

Aged Mortgage Leads - Suggested Scripting #2 Firms are usually...