By James Schulze

This article discusses how the current Iran conflict is causing a shift in how modern consumers view energy and the value that solar solutions can offer them. It also highlights how solar installers can modify their messaging to better tap into these psychological shifts in consumers, ultimately driving up sales.

The ongoing conflict involving Iran is far more than a localized geopolitical flashpoint or a temporary disruption to the status quo. It represents a profound, systemic reminder of just how fragile, interconnected, and fundamentally vulnerable the global energy architecture remains today. For decades, the modern world has operated under the assumption of seamless supply chains, but recent macroeconomic shocks are forcing a harsh re-evaluation.

According to a detailed analysis by Wood Mackenzie, a prolonged disruption passing through the critical transit pathway of the Strait of Hormuz has the potential to remove over 11 million barrels of oil per day from global markets. Simultaneously, such an event would choke off roughly 20% of the world’s liquefied natural gas (LNG) supply.

While these staggering figures dominate the terminal screens of commodity traders and consume the attention of foreign policy officials, their ultimate impact reaches far beyond government briefings and Wall Street trading floors. They matter immensely to regular homeowners sitting at their kitchen tables. Quietly but forcefully, this macroeconomic instability is poised to become one of the most powerful long-term catalysts for residential solar and battery storage adoption over the next decade.

The Strait of Hormuz and consumer consciousness

Most Americans do not spend their mornings pondering the logistics of Middle Eastern energy chokepoints or analyzing shipping lanes. Yet, they feel the ripple effects of those structural vulnerabilities constantly. The Strait of Hormuz remains one of the most vital, irreplaceable energy arteries on Earth. When instability strikes the region, global oil and gas prices react instantly and aggressively. Wood Mackenzie warns that if these disruptions continue to persist, global energy markets could face the single largest supply shock witnessed in over a century.

This is no longer a theoretical exercise or a worst-case scenario confined to academic whitepapers. European consumers already experienced a painful, real-world preview of this exact dynamic in the wake of Russia’s invasion of Ukraine. As global energy prices surged and governments scrambled to secure replacement of LNG cargo, systemic vulnerabilities were laid bare. Coal plants were forced to stay online far longer than climate targets expected, and consumers suddenly underwent a massive psychological shift, becoming acutely aware of exactly where their energy actually originates.

Now, the conflict involving Iran has reopened that exact conversation on a global scale, forcing a macroeconomic reality check onto the domestic consumer.

The modern energy consumer

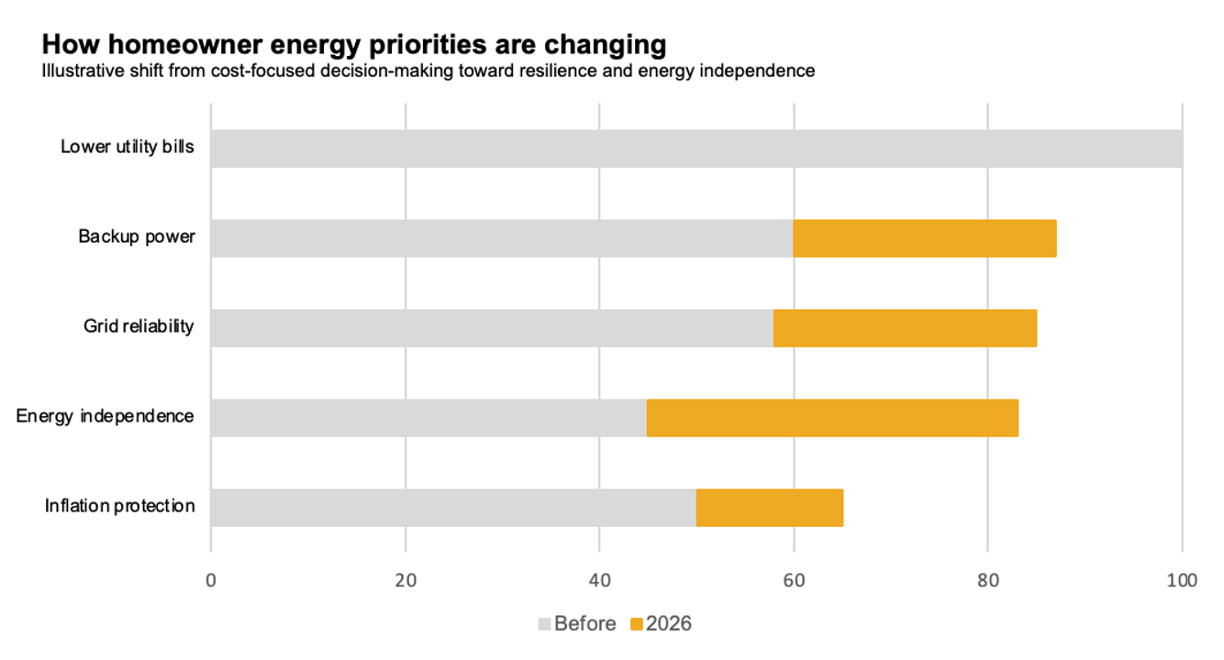

Historically, the residential solar industry relied on a highly predictable, one-dimensional marketing playbook centered almost exclusively on immediate financial savings a homeowner could realize. While lowering a homeowner’s monthly utility bill still carries weight, the modern homeowner’s motivation has evolved past mere financial arbitrage. Increasingly, consumers are reacting to a compounding mix of domestic anxieties:

- Widespread grid instability

- Frequent and prolonged blackout concerns

- Growing distrust of centralized utilities

- Systemic inflation that erodes purchasing power

As a result, battery backup systems are no longer viewed as a luxury add-on but as a fundamental component of long-term household resilience.

This represents a profound psychological shift. The modern consumer increasingly demands attributes that traditional utilities simply cannot guarantee, like absolute control over their power generation, pricing stability in an inflationary environment, predictability of long-term costs, and ironclad protection from global market volatility.

This completely changes the residential solar conversation. The strongest, most successful solar companies are no longer just pitching a lower monthly bill. Instead, they are actively selling:

- Energy independence

- Absolute household resiliency

- Reliable backup protection

- Insulation from global uncertainty

The choice of “molecules versus electrons”

One of the most critical sections highlighted in the Wood Mackenzie analysis is framed as a civilizational choice: “molecules versus electrons.” The core argument put forth by analysts is elegant and sweeping: countries that find themselves structurally dependent on imported oil and gas–the molecules–will be forced to aggressively pursue rapid electrification policies–the electrons–as a direct national security response to geopolitical instability.

In practice, this systemic pivot manifests as an accelerated, state-backed transition toward:

- Rapid electric vehicle (EV) adoption to choke off oil reliance

- Massive capital deployment into battery storage and comprehensive grid modernization

- Aggressive expansion of large-scale renewable utility assets

- Widespread transition to electrified heating infrastructures to bypass natural gas dependence

- Optimization of localized, distributed energy systems

The report specifically notes that Europe is highly likely to accelerate its deployment of solar, wind, storage, and grid modernization if this geopolitical instability persists. At the macro level, this is fundamentally an issue of national energy security and sovereign defense. However, when filtered down to the residential level, this exact same macro trend directly supports the long-term investment thesis for rooftop solar, home batteries, distributed generation assets, and fully electrified homes.

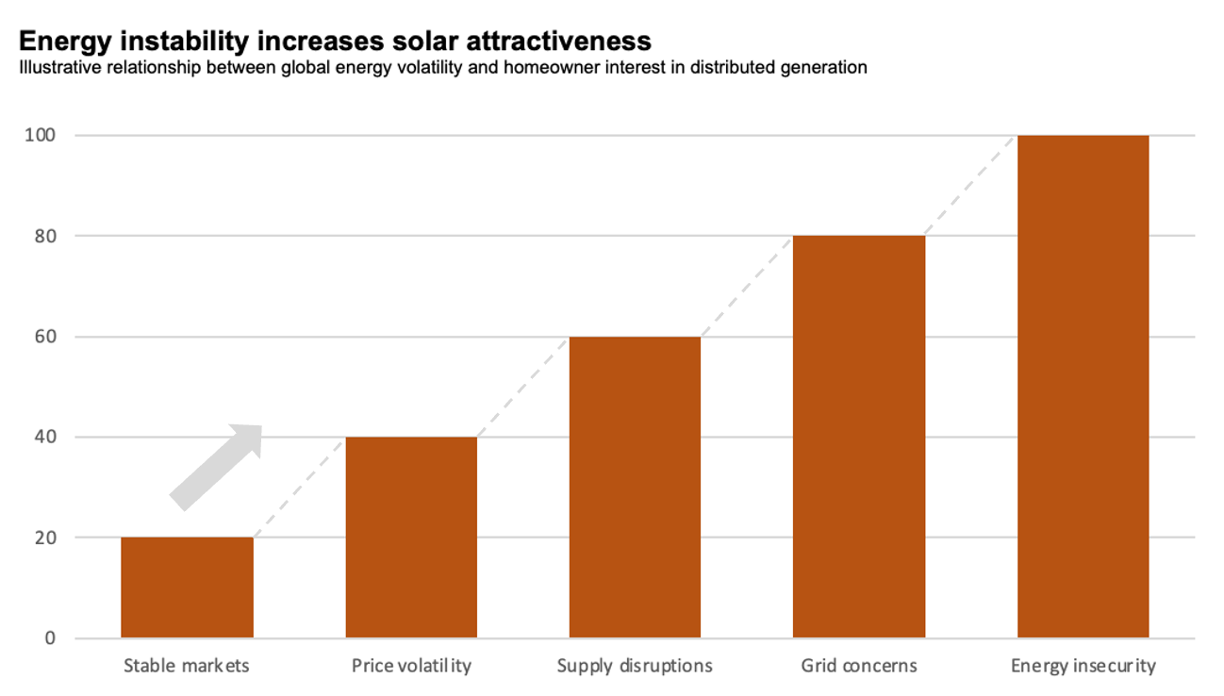

In other words, a direct mathematical correlation is emerging: the less stable and more volatile global hydrocarbon markets become, the more financially and operationally attractive localized, onsite electricity generation becomes to the individual consumer.

Solar as a resiliency product

This is precisely where the vast majority of local solar installation companies are lagging behind the cultural curve. Much of the current installer marketing and lead generation copy looks virtually identical to how it did years ago, stubbornly leaning on legacy financial hooks: “lower your bill,” “lock in your rates,” “no money down,” and “save money monthly.”

While that transactional messaging still captures a segment of the market, it fails to address the deeper cultural shift. The next structural evolution of the residential solar sector will increasingly revolve around themes of absolute reliability, total self-sufficiency, robust backup capability, and deliberate insulation from geopolitical instability.

We have already witnessed localized, regional previews of this psychological transition across the United States. California homeowners aggressively adopted solar-plus-storage systems not out of altruism, but as a direct survival mechanism against wildfire-induced public safety power shutoffs and unpredictable rolling blackouts. Similarly, Texas consumers underwent a rapid awakening regarding the vulnerability of their independent grid during the catastrophic infrastructure failures of Winter Storm Uri.

Through these crises, consumers are rapidly internalizing a vital truth: cheap electricity and reliable electricity are no longer guaranteed to be the same thing. This realization marks a permanent psychological shift in how the average citizen values energy infrastructure.

But there is a catch: supply chain contractions

An objective analysis requires acknowledging a stark, deeply ironic challenge embedded within this thesis. The very same geopolitical friction that is supercharging long-term consumer demand is simultaneously creating severe operational challenges for the solar industry’s manufacturing base.

Wood Mackenzie points out a troubling reality: the current conflict has already directly delayed or outright canceled more than 30 GW of planned solar module manufacturing capacity globally. Furthermore, global battery storage shipments have already been revised downward by a staggering 25%. For solar operators on the ground, this supply-side contraction translates directly into a difficult operating environment characterized by:

- Significantly higher upfront equipment and procurement costs

- Severe financing pressures driven by capital market volatility and risk aversion

- Extended supply chain delays and frustrating installation bottlenecks

- Unpredictable pricing volatility that makes long-term project budgeting difficult

Consequently, the industry is entering a period of intense structural tension. The exact same global instability that solidifies long-term consumer adoption is simultaneously complicating the near-term economics of deploying those systems. Navigating this delicate friction is likely to be the defining challenge for renewable energy executives over the next several years.

The macro perspective: crisis as a catalyst for solar adoption

When viewed through the lens of economic history, major energy shocks have repeatedly functioned as the primary accelerators for sweeping energy transitions. The severe oil crises of the 1970s permanently reshaped global energy policy, birthed modern fuel efficiency standards, and catalyzed the first serious Western investments in domestic alternative energy. Decades later, Russia’s actions in 2022 permanently broke Europe’s reliance on pipeline gas and compressed a decade’s worth of renewable policy deployment into a matter of months.

Now, the conflict involving Iran further reinforces the foundational premise that import-dependent economies simply cannot rely indefinitely on fragile, highly volatile global hydrocarbon supply chains.

Residential solar sits directly in the center of this historical macroeconomic current. This isn’t occurring because the average suburban homeowner is suddenly studying Middle Eastern geopolitical maps or tracking oil tankers through the Strait of Hormuz. It is occurring because global energy insecurity is a fluid entity that eventually knocks on every citizen’s door. It inevitably manifests in escalating utility bills, on nightly television broadcasts, in generalized inflation metrics, during physical grid outages, and deep inside localized consumer anxiety.

Ultimately, consumer anxiety is what drives and reshapes massive markets. While lead generation mechanics, competitive pricing structures, and creating financing products will always matter to an installer’s balance sheet, the companies that win the next decade will be those that look beneath the surface. They will be the organizations that speak directly to the core emotional drivers emerging in the modern market: security, reliability, control, independence, and resilience. Many solar companies still mistakenly believe their primary product is financial savings. Increasingly, their true product is energy stability in a fundamentally unstable world.

About the author

James Schulze is the President and CEO of The Leads Warehouse, a marketing data company with over 20 years of experience in bringing lead generation solutions to companies selling into the home, automotive, financial, insurance, health and life, and legal sectors. He works directly with clients to optimize conversion strategies and ROI across multiple verticals.

Connect with James Schulze on LinkedIn:

https://www.linkedin.com/in/james-l-schulze

Read additional market analysis and commentary from James Schulze on Substack:

https://jameslschulze.substack.com

If you are serious about improving your solar leads strategy, a strong mix of leads is important. Our team works with solar installers to maximize their ROI on solar sales leads. Call 1-800-884-8371 or visit The Leads Warehouse to get started.